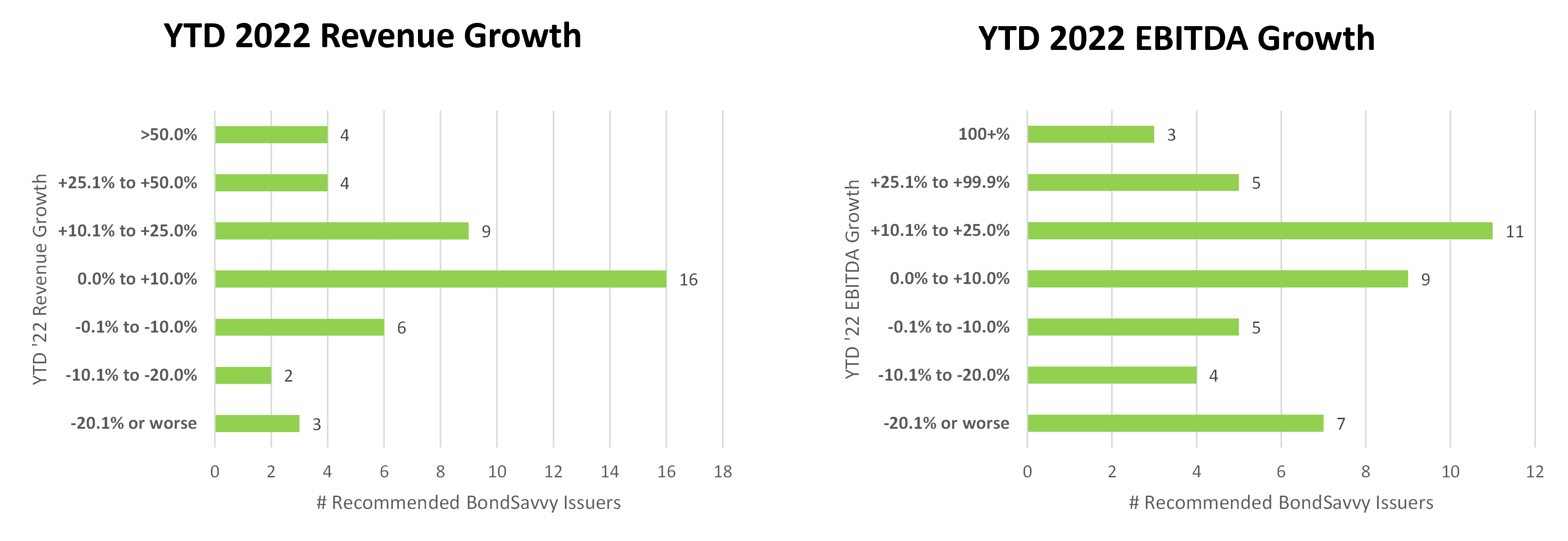

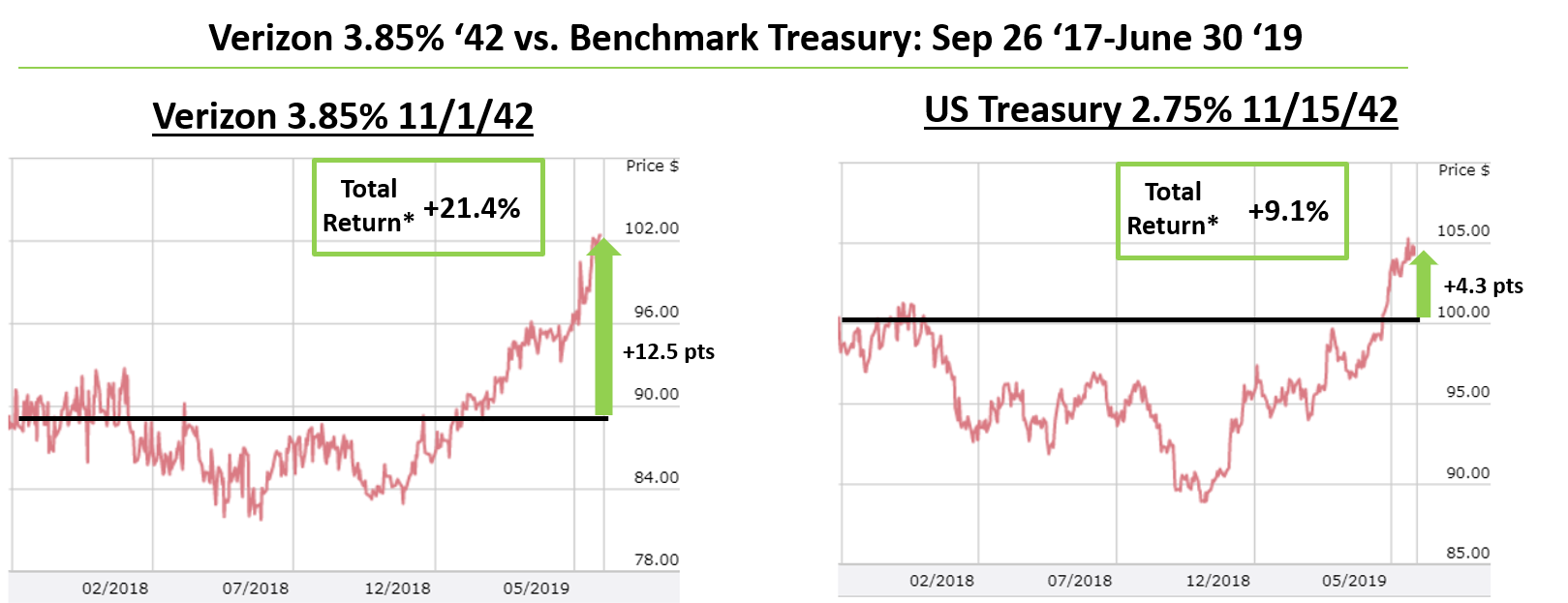

Through July 31, 2023, Bondsavvy had made 113 corporate bond recommendations. These include 59 individual bonds we currently recommend as buy (32) or hold (27) and 54 bonds we previously recommended but have since recommended selling. This corporate bond returns update discusses the drivers of the performance of the 59 corporate bonds we currently rate either buy or hold.Corporate Bond Returns of Our Last Five Sets of Recommendations Bondsavvy presents subscribers new corporate bond recommendations during The...

4 min readThrough July 31, 2023, Bondsavvy had made 113 corporate bond recommendations. These include 59 individual bonds we currently recommend as buy (32) or hold (27) and 54 bonds we previously recommended but have since recommended selling. This corporate bond returns update discusses the drivers of the performance of the 59 corporate bonds we currently rate either buy or hold.

Corporate Bond Returns of Our Last Five Sets of Recommendations

Bondsavvy presents subscribers new corporate bond recommendations during The Bondcast, a quarterly live webcast that includes subscriber questions and answers. During each edition of The Bondcast, we typically present four to six new corporate bond recommendations.

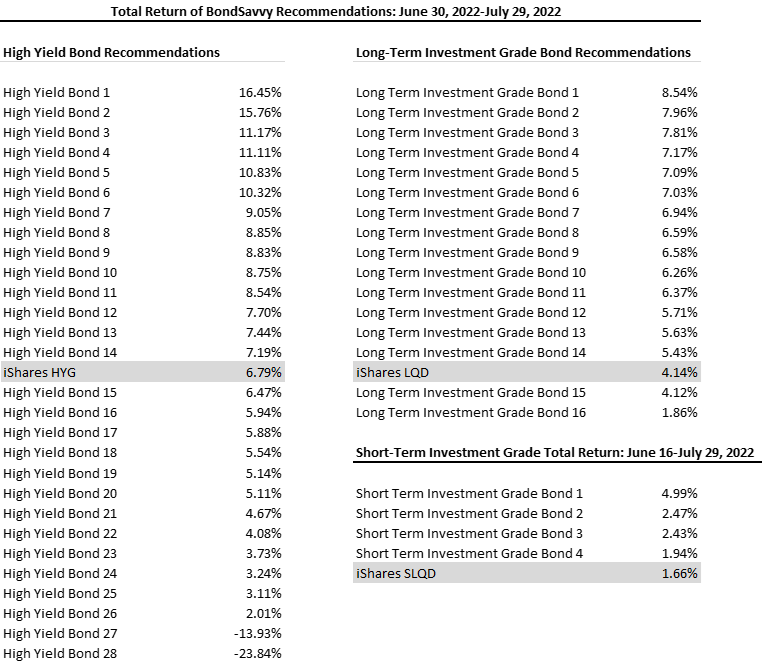

We made our last five sets of recommendations on June 22, 2023, March 8, 2023, November 16, 2022, June 16, 2022, and April 6, 2022. You can see the corporate bond returns of these and all other investment recommendations in the above tables.

Given how aggressive the Federal Reserve was with increasing interest rates starting in early 2022, our recent recommendations were primarily bonds with high yield bond ratings and short term investment grade bonds. These bonds are generally less sensitive to movements in the US federal funds rate.

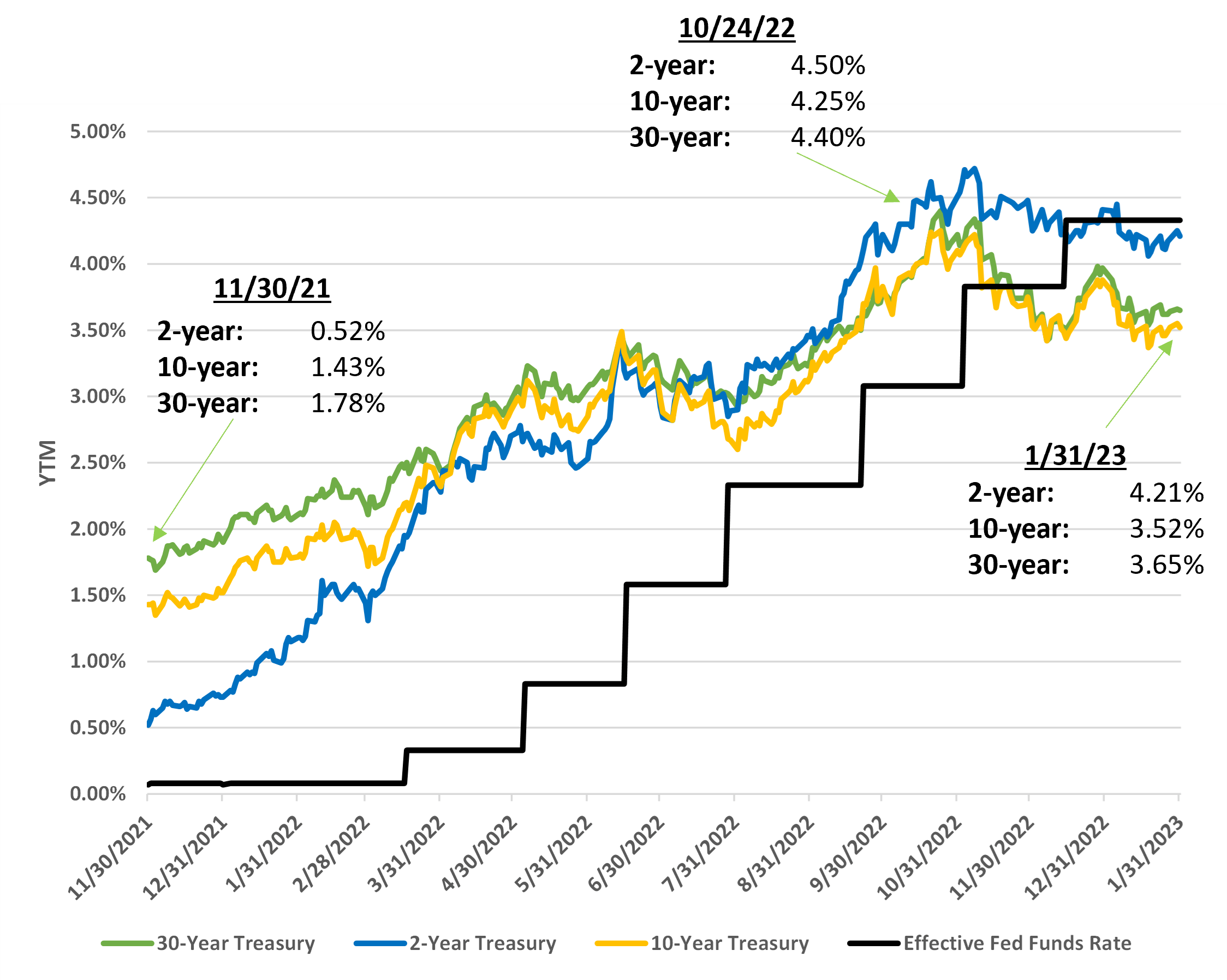

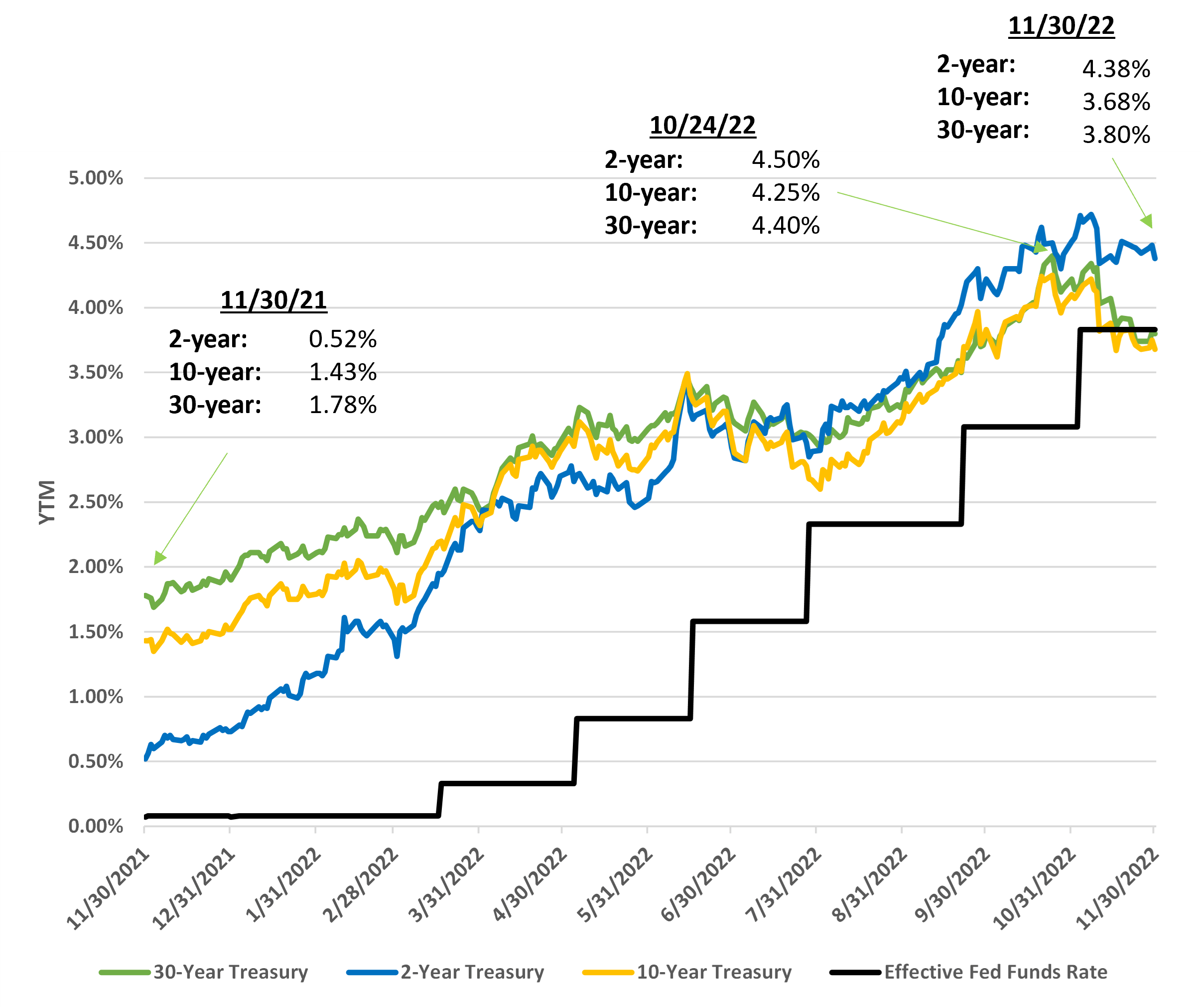

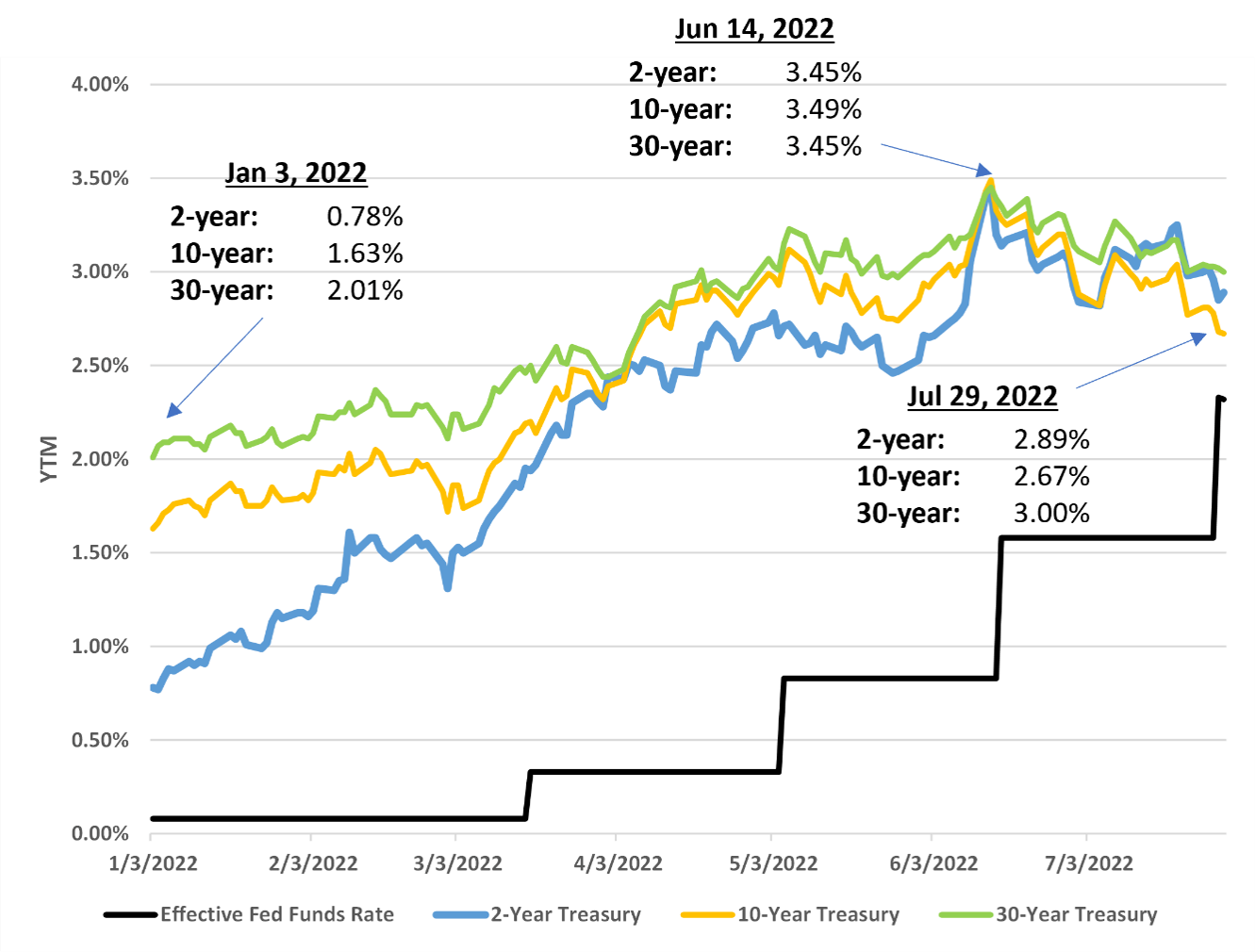

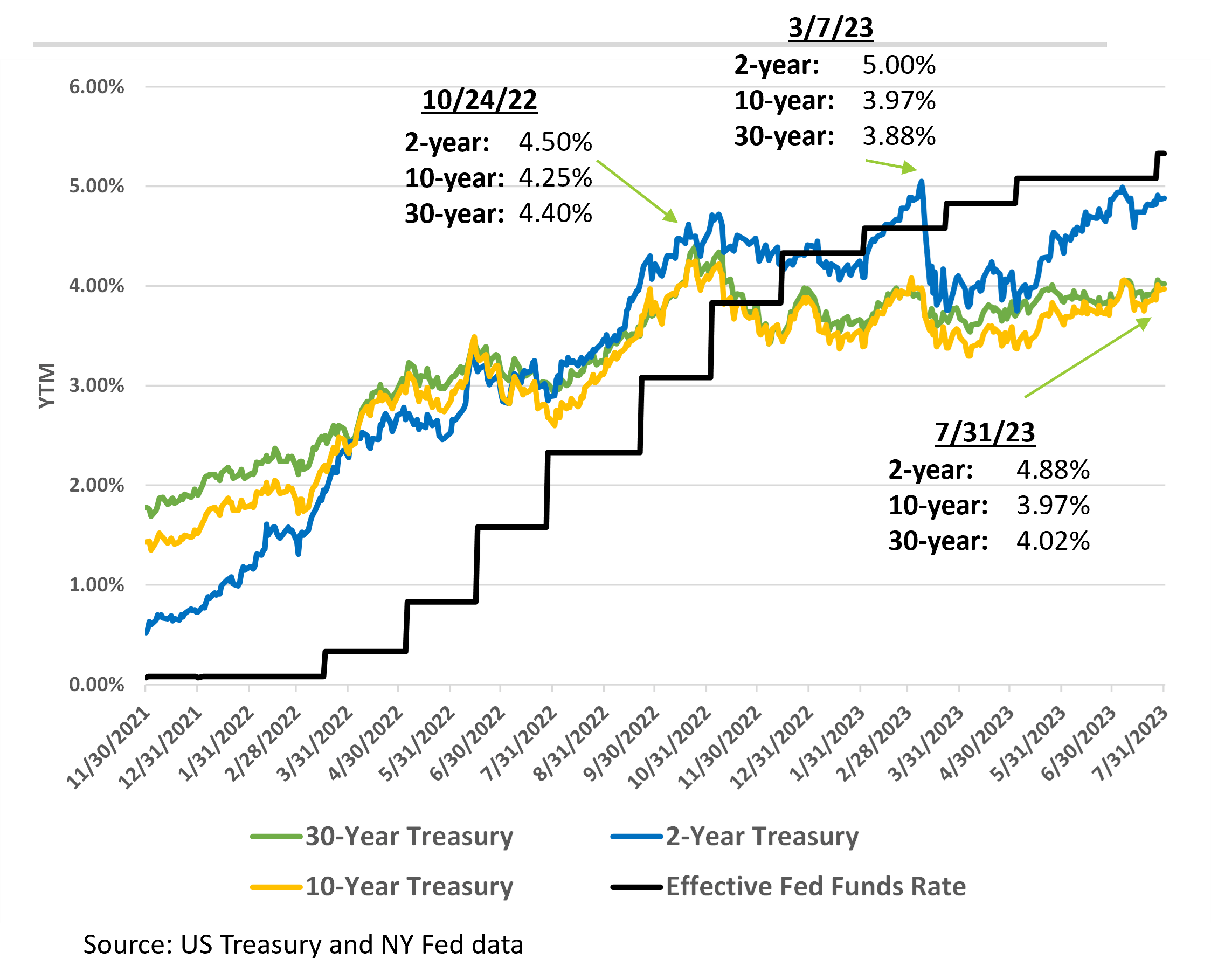

As we discuss in our corporate bond credit spreads blog post, corporate bond yields to maturity (YTM) are driven by the "benchmark US Treasury YTM" and the corporate bond's credit spread. The benchmark US Treasury yield is the YTM of a US Treasury note, bond, or bill that has a similar maturity date to a specific corporate bond. The smaller a corporate bond's credit spread is to its YTM will make that bond more sensitive to movements in US Treasury yields vs. changes in credit spreads. For example, YTM movements of a corporate bond with a 5.00% YTM and a 0.50% credit spread will generally be driven more by changes in US Treasury yields than in changes in credit spreads.

Figure 1 compares the effective federal funds rate to the YTMs of the 2 year Treasury, 10 year Treasury, and 30 year Treasury. As the Federal Reserve kept increasing the federal funds rate (black bar), US Treasury yields largely followed suit until late 2022. There was then a divergence between short- and long-term US Treasury yields, as the 2 year Treasury continued increasing to 5.00% on March 7, 2023, while the 10 year Treasury and 30 year Treasury YTM have generally been trading between 3.30% to 4.00% since January 1, 2023.

Figure 1: US Treasury Yields vs. the Effective Federal Funds Rate -- November 30, 2021-July 31, 2023

The good news

The good news is that -- compared to 2022 -- bond markets have generally stabilized. Of our 23 most recent bond recommendations, 19 (83%) have been profitable thus far. As these investment recommendations were made between April 6, 2022 and June 22, 2023, we are still early in our likely holding period of these bonds. While it is way too early to declare any of these investments an ultimate success, we are pleased that our recent recommendations have made money in a difficult environment for bonds.

Please note that, within the 23 recommendations, there was one bond we recommended selling on July 13, 2023. This was the Mercer International 5.125% 2/1/29 bond (CUSIP 588056BB6), which had a terrible Q1 2023 and, when sold, recorded a -0.73% total return.

The bad news

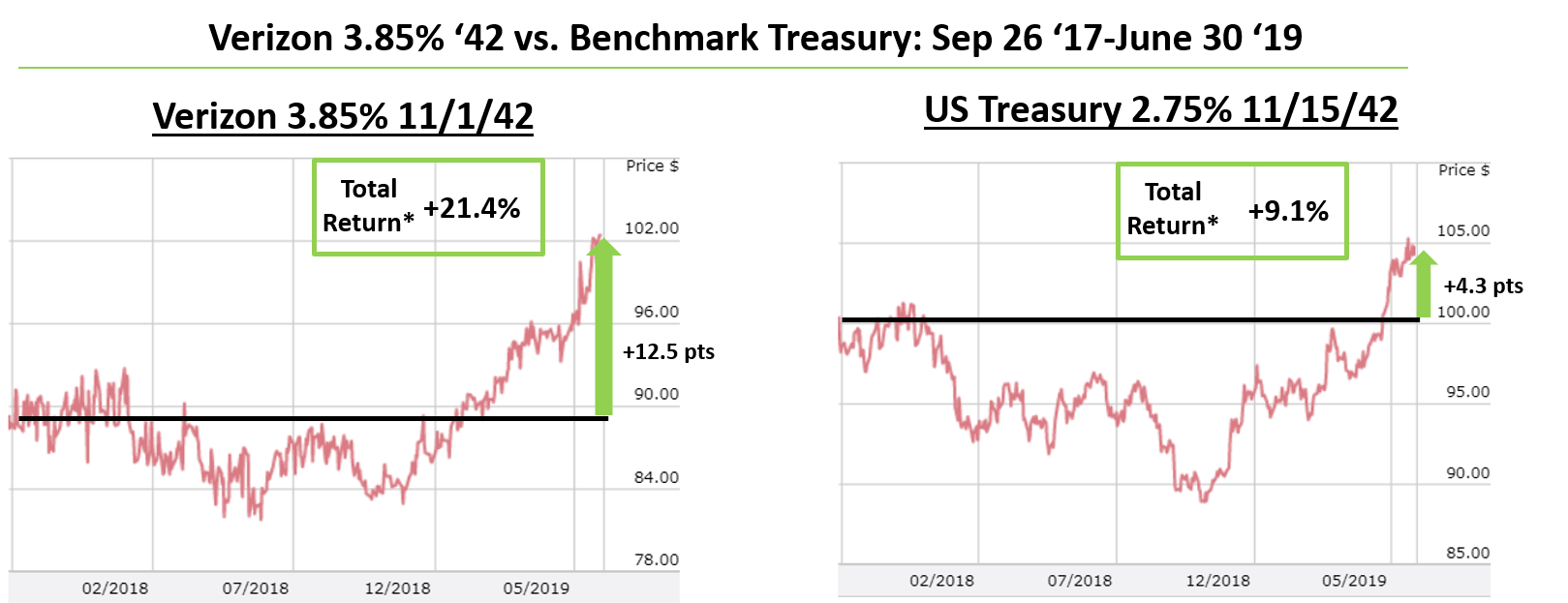

While there were some bright spots, many picks made between September 23, 2020 and January 12, 2022 have delivered weak performance. These bond recommendations were made when US Treasury yields were extremely low. As Treasury yields rose, many of these bonds, especially long-dated investment grade corporate bonds, fell sharply. Since long-term investment grade corporate bonds are heavily impacted by changes in long-dated US Treasury yields, we believe it will take some time for these bonds to recover in price.

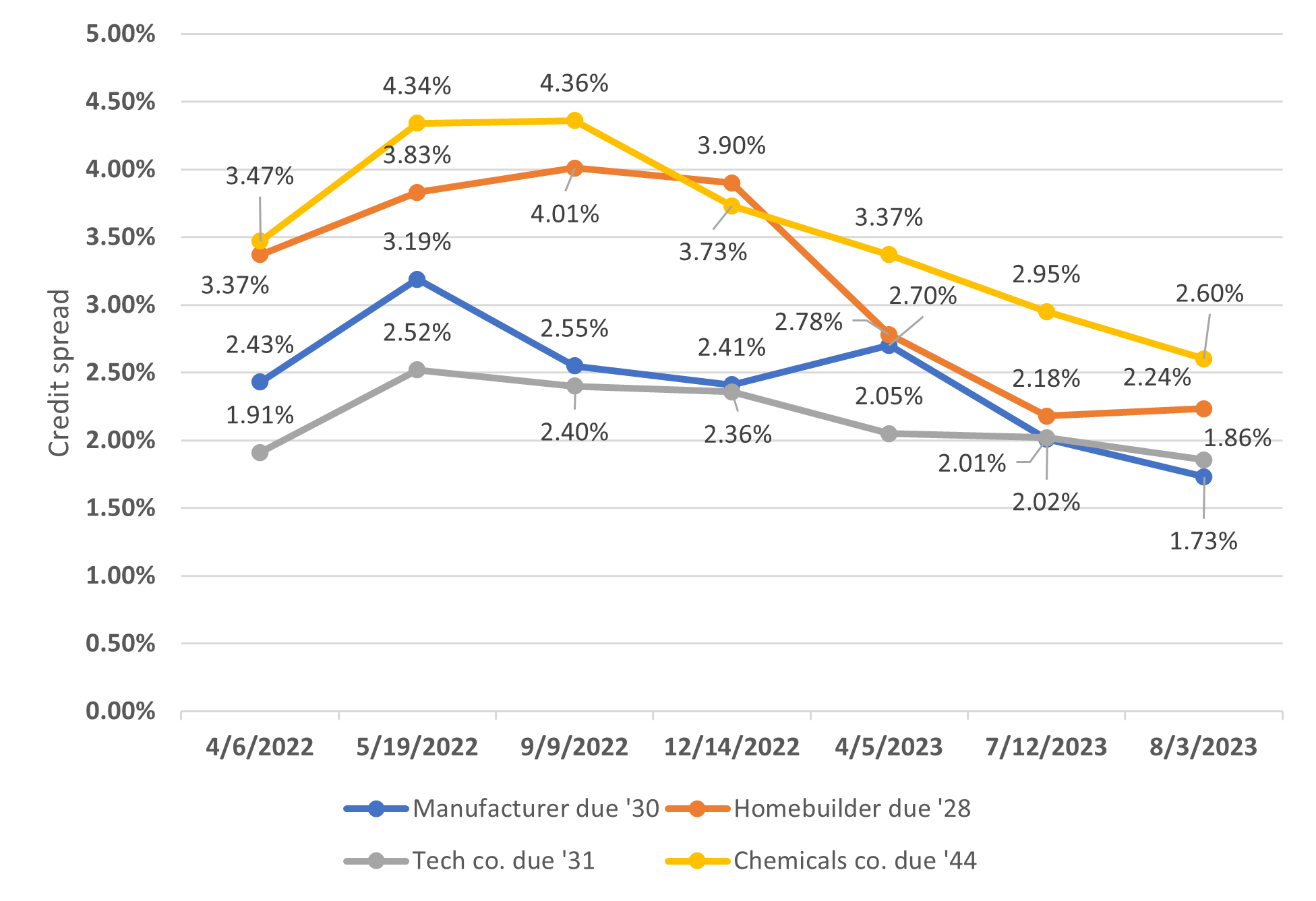

Recent Movements in US Corporate Bond Credit Spreads

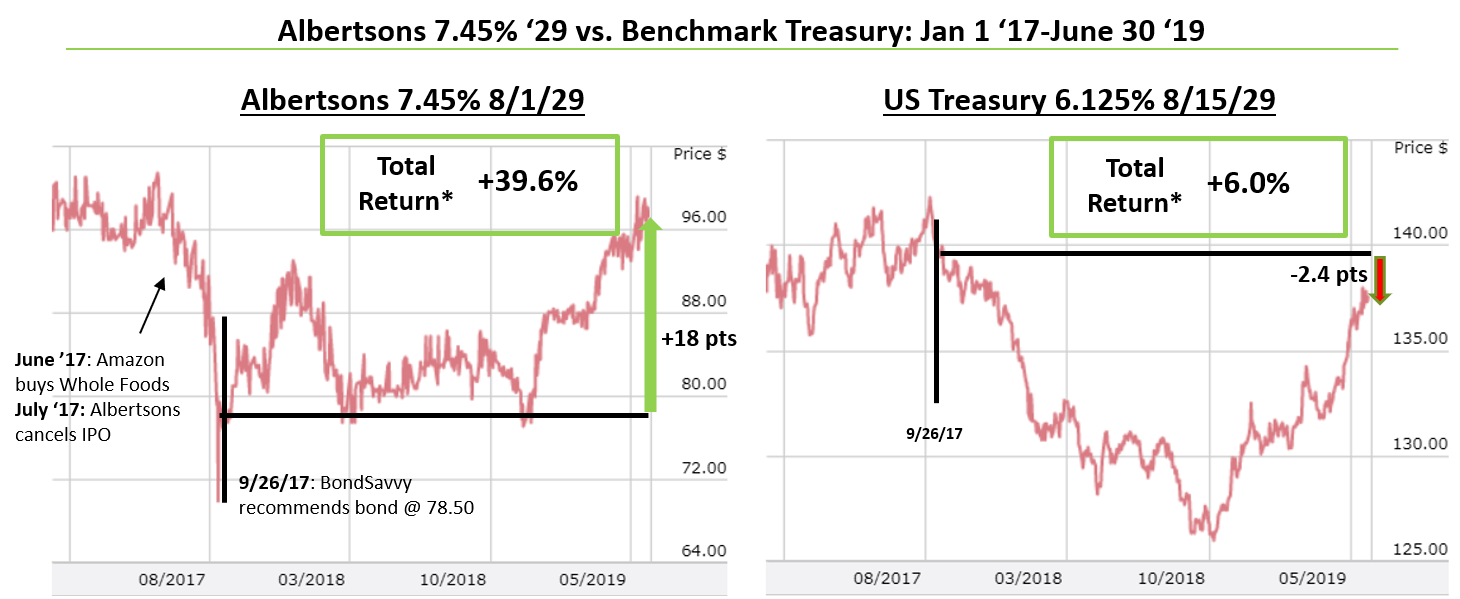

If a corporate bond has a high credit spread relative to a bond issuer's underlying financials, that bond generally has a good value. Identifying these undervalued corporate bonds is a key Bondsavvy focus when we make new corporate bond recommendations.

Figure 2 tracks the historical credit spreads of four high yield corporate bonds we recommended April 6, 2022. In Figure 2's legend, we provide generic information about each bond, including the issuer's industry and the bond's maturity date. Subscribe to Bondsavvy to learn the names and CUSIPs of all Bondsavvy investment recommendations.

As shown in Figure 2, the credit spreads of these four high yield bonds generally moved up from the April 6, 2022 pick date until May 19, 2022, when we provided our quarterly recommendations update on The Super Bondcast. These credit spreads have generally trended lower since September 9, 2022. As of August 3, 2023, the credit spread of each of the four bonds was lower than it was on the April 6, 2022 pick date.

Figure 2: Historical Corporate Bond Credit Spreads of Four Recent Bondsavvy Recommendations -- April 6, 2022-August 3, 2023

What do these changes in credit spreads mean?

Even if underlying US Treasury yields are rising, a corporate bond's price can still increase if the credit spread falls by an amount greater than the benchmark Treasury YTM. For several months after we issued these four recommendations, US Treasury yields rose and credit spreads rose. This "double whammy" caused these high yield bond prices to fall. The bonds have subsequently recovered some of their value, as the US Treasury market has stabilized and credit spreads for these bonds have fallen.

While falling credit spreads has been a good thing for these bonds, it does mean that a buyer of these bonds today will generally have less capital appreciation opportunity than buyers of the bonds in May 2022 when credit spreads were higher. When credit spreads are relatively high, it means they have more room to fall. The more a credit spread falls (assuming no change in underlying US Treasury yields), the more a corporate bond price can increase.